For the last number of decades, the real estate market has been broken down into seasons with spring reigning as the best time to sell a home. Traditionally, that’s how it’s been. But there’s a big shift happening now.

Recent years have seen that seasonality blur as more and more people decide to buy or sell a home no matter what time of year it is.

What we do know is that while we’ll probably see more homes hit the market this spring, supply is still too low to keep up with demand.

So, even if more homes do come on the market compared to previous months, there are plenty of willing and ready buyers waiting on the sidelines to scoop them up.

WHY ARE PRICES RISING SO QUICKLY?

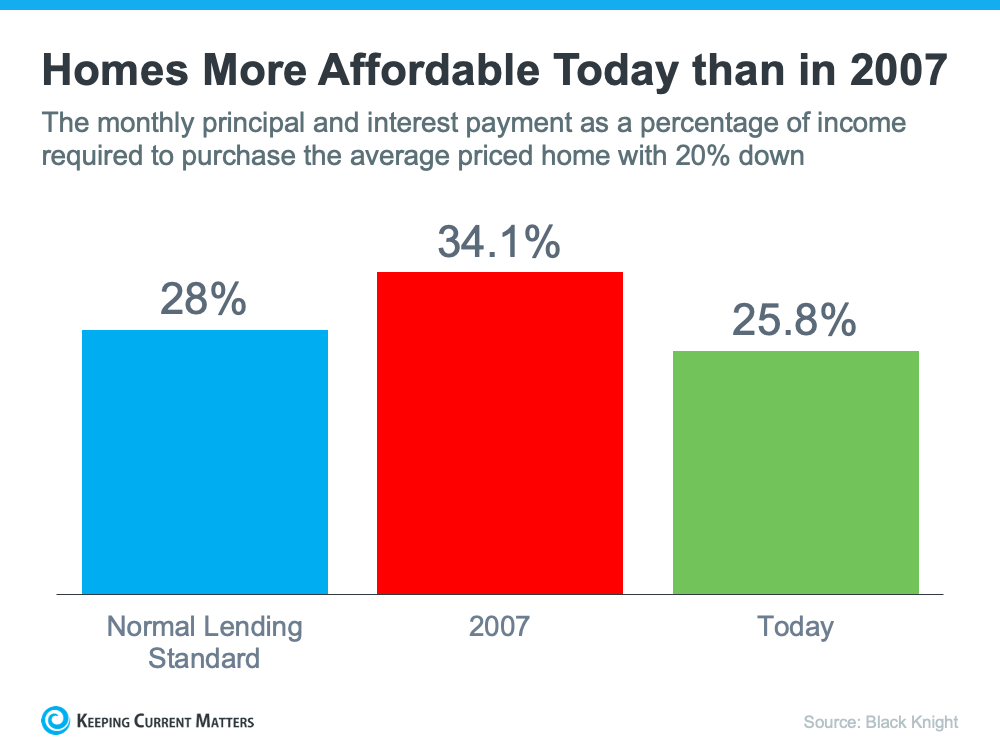

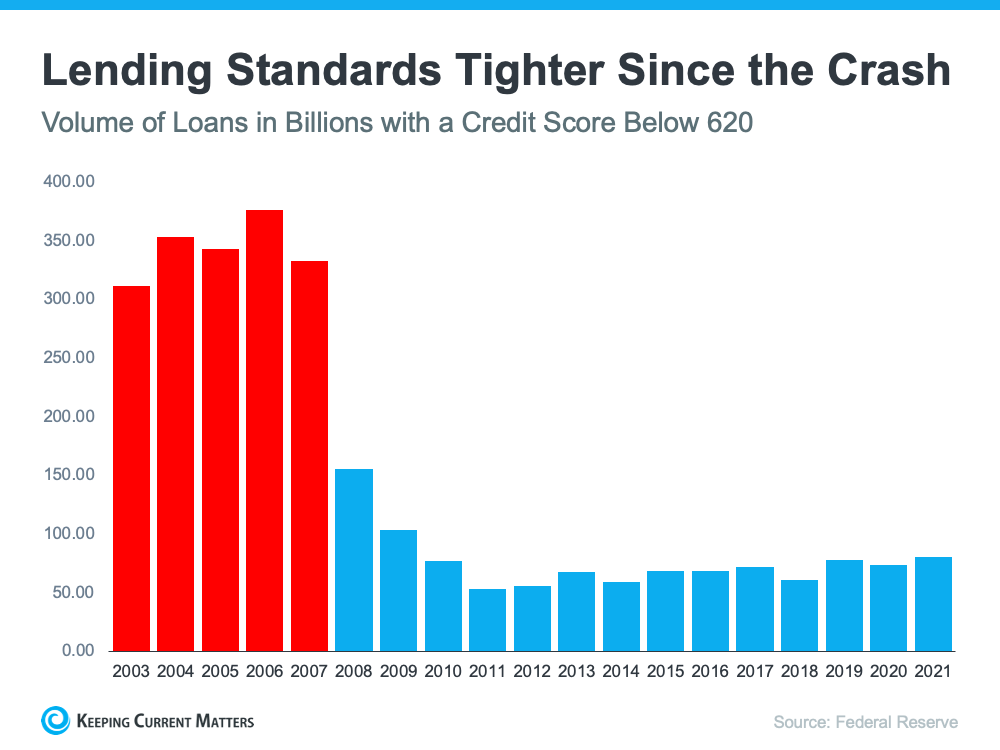

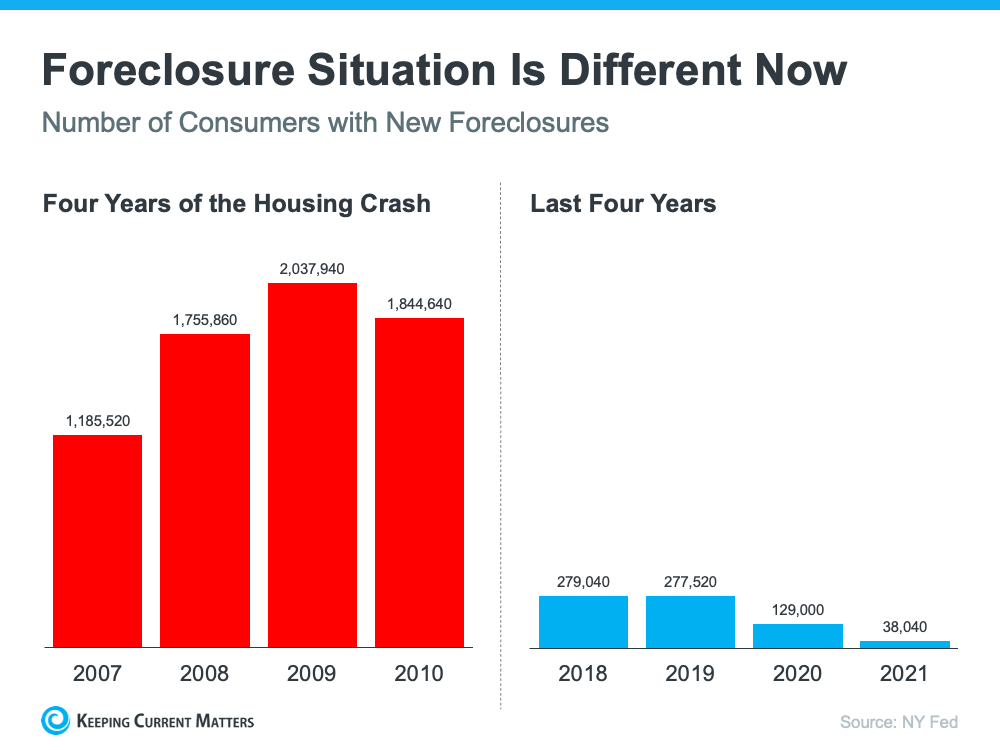

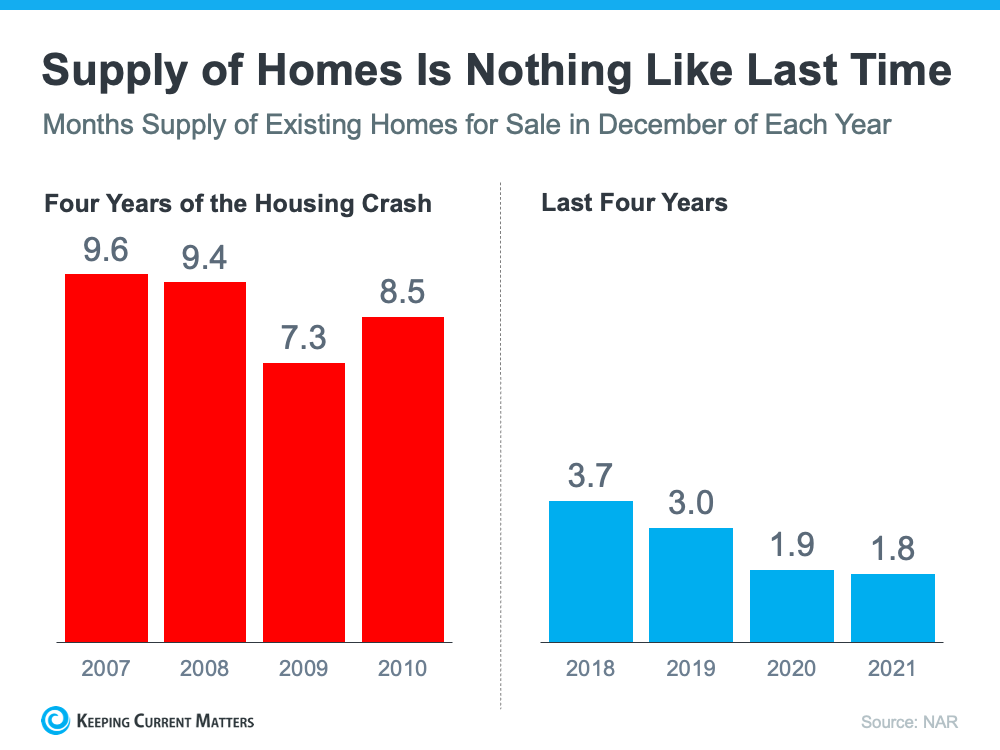

No one wants to buy at the top of the market. We saw how that played out in 2008, and it didn’t end well for a lot of homeowners.

But according to recent expert projections, we aren’t at the top of the market.

But before we dive a little deeper into that, we need to explain a couple of things.

First, with both Millenials and Gen Z now in the buyer group, there isn’t enough existing inventory to keep up with the amount of aspiring homeowners. Second, we didn’t build enough homes in the last decade to keep up with the demand.

This leads us directly to our next big question.

SHOULD I WAIT TO BUY UNTIL PRICES GO DOWN?

So, with existing inventory not being able to keep up with the number of buyers looking to own a home, we are seeing price appreciation that looks strikingly similar to what we saw in the years leading up to the crash.

The big difference between now and then is this: this price appreciation is a direct result of low inventory and high demand. Not high inventory and high demand like in the early 2000s.

Plus, earlier projections by top industry experts are already being revised to higher than originally anticipated. That means more likely than not, we could see another year of above-average price appreciation.

HOW WILL RISING INFLATION IMPACT THE HOUSING MARKET?

Inflation: one of the most unfortunate results of the pandemic. And there have obviously been many (let’s never forget the infamous toilet paper shortage).

But inflation isn’t new. And if we look all the way back to 1970, we actually see one big takeaway: homeownership is historically a great hedge against it.

For example, as rental prices continue to rise nationwide, locking in mortgage payments can keep your largest monthly cost the same. remain the same.

Another big takeaway: home price appreciation has outperformed inflation for decades.

So, if you are worried about how today’s inflation may affect the housing market : at the very least, data shows that historically real estate has outperformed inflation.

SHOULD I WAIT UNTIL PRICES GO DOWN TO BUY?

Like we covered above, industry experts are projecting that prices will only go up from here (and that’s not likely to change anytime soon).

There are many benefits to homeownership. But the biggest one you need to consider right now is that it’s consistently been voted the best long-term investment a person can make in their life.

And waiting for the market to cool off or prices to go down means only one thing: paying more for the exact same house. Especially as experts project mortgage rates will continue to rise.

The best advice I can give to those who are hesitant to hop into this hot market is this: you can wait, but it will probably cost you.

Bottom Line

If you have questions about this market, I am here to be your trusted resource. Let’s at least have a conversation about your situation and see if I can be of service.

Lesley Lambert, Western MA REALTOR with Park Square Realty 413-575-3611

source credit: https://www.keepingcurrentmatters.com/article/the-biggest-questions-clients-are-asking-this-spring/?utm_campaign=2203_5_Slides&utm_medium=email&utm_source=email-broadcast&utm_content=Blog_Digest&utm_term=agent_article&source=